The Entrepreneurship Issue

Navigating the Choppy Waters Ahead for 2025

As we look toward 2025, there are five key trends that we believe will shape the direction of global higher education policy. These trends highlight both opportunities and challenges, and understanding their implications will be critical for navigating the uncertain waters ahead.

- The Growth of International Student Mobility

According to research from Holon IQ, the number of international students seeking overseas education is expected to rise significantly to 7 million by the end of the decade. While the market itself is growing, traditional English-speaking destinations—including Australia, Canada, the UK, and the USA — are experiencing a decline in market share.

Emerging destinations in Asia, Europe, and the Middle East are poised to benefit from this shift. These regions are capitalising on the uncertainty and perceived unwelcoming environments in major English-speaking countries, offering attractive alternatives for international students. As a result, we anticipate a redistribution of international student flows, with increasing numbers choosing these emerging study destinations over traditional ones.

- Intensifying Anti-Immigration Policies

A growing wave of anti-immigration sentiment is expected to further complicate international student recruitment in 2025. Hostile policies, restrictive visa regulations, and nationalist rhetoric are becoming more prevalent in major host countries. This is particularly concerning given the upcoming general elections in Australia and Canada, as well as a Trump presidency in the United States. These developments are likely to exacerbate existing challenges.

Issues such as housing shortages and strained public services will continue to dominate public discourse, with international students often serving as convenient scapegoats. These factors will undoubtedly impact the attractiveness of traditional study destinations and could lead to a decline in international enrolments in these regions.

- The Deepening University Funding Crisis

The financial challenges facing universities are set to intensify. Funding crises, exacerbated by inflation and cuts to government support, will lead to significant restructuring within the higher education sector. University mergers are expected to become more common, and a small number of institutions may cease operations altogether. The fallout from such closures — including job losses, economic disruption in local communities, and challenges in accommodating current students — will have profound and long-lasting implications.

Moreover, the reputational damage to national higher education systems could deter future international students, further aggravating the funding crisis. Addressing these issues will require bold and innovative solutions from universities and policymakers alike.

- Increasing Regulation of Agents and Aggregators

Governments in key study destinations are taking steps to regulate the role of agents and aggregators in international student recruitment. Recent measures, such as the mandatory listing of agents on Confirmation of Acceptance for Studies (CAS) forms in the UK, as well as enhanced regulations in Australia and Canada, reflect a broader push for transparency and accountability.

While we have long advocated for transparency in international recruitment, the lack of self-regulation within the sector has forced governments to intervene. These regulatory measures are a step toward restoring trust and ensuring that recruitment practices align with ethical standards. However, universities must proactively adapt to these changes to avoid potential pitfalls and maintain their competitive edge.

- Shifting Dynamics in Key Source Countries

China and India, the world’s two largest source countries for international students, are undergoing significant changes that necessitate a re-evaluation of recruitment strategies. Students from these regions are increasingly seeking outcomes that align with their specific motivations and goals, rendering a one-size-fits-all approach ineffective.

In China, where parents often fund their children’s overseas education, many graduates traditionally return home to pursue careers. However, rising unemployment rates in mainland China could alter this trend, prompting some graduates to explore opportunities abroad. In contrast, Indian students, who are largely reliant on bank loans to finance their education, prioritize post-graduate work opportunities in their host countries to repay these loans. This focus on employment prospects underscores the need for targeted strategies that address these differing priorities.

Both groups require nuanced recruitment approaches that reflect their unique motivations and provide realistic expectations based on international graduate outcomes data. Universities must tailor their messaging and support services accordingly to remain competitive.

Strategies for Navigating the Challenges of 2025

Given the stormy waters ahead, how should higher education institutions adapt to what promises to be an increasingly challenging environment? One key strategy is for universities, particularly those seeking to expand their international student populations, to focus on employability outcomes in students' home countries.

Addressing Anti-Immigration Sentiment

The root cause of restrictive government policies is often widespread public discontent with immigration. Although these concerns are frequently unfounded, immigration remains a central issue in election campaigns across the West. Universities must respond by shifting their emphasis away from post-study work opportunities as the primary selling point for international students. Instead, they should prioritise supporting graduates in transitioning to successful careers in their home countries.

While this is not an either/or scenario, universities must recognize the limitations of current approaches. Careers services are already doing commendable work in helping international graduates find employment locally. However, significant barriers remain, including the high costs and bureaucratic hurdles associated with sponsorship and securing skilled work visas and increasing salary thresholds for eligibility. As a result, only a small percentage of international graduates are likely to secure long-term employment in their host countries, even when we take into account post-study work opportunities.

Investing in International Graduate Support

Given the challenges associated with securing permanent residency or long-term employment in host countries, universities must invest in resources to help international students navigate their home labour markets. This could involve enhancing the capacity of international offices and career services, which would require only minimal investment relative to a single tuition fee generated by an international student and redeployment of one or two staff to focus on successful international graduate outcomes and engage with overseas employers.

Failure to address these needs could damage the reputation of traditional study destinations. When returning graduates struggle to find employment, they are likely to share their dissatisfaction through social media and other platforms. This is already evident in China, where rising domestic unemployment and scepticism about the value of overseas degrees are prompting students to consider more affordable options closer to home.

Leveraging Data and Industry Partnerships

By focusing on international graduate outcomes, universities can complete the student lifecycle—from recruitment to education and employment. Collecting and analysing data on graduate destinations and career trajectories can provide valuable insights into the long-term value of an overseas degree. This data can also help institutions strengthen relationships with industry partners, offering opportunities for talent pipelines, professional development programs, and applied research collaborations.

Moreover, robust outcomes data can serve as a powerful tool for lobbying governments and addressing regulatory challenges. Demonstrating that the majority of international students go on to successful careers in their home countries, can counter negative narratives about immigration and support the case for continued investment in international education. Additionally, this data can facilitate trade and foreign direct investment by fostering connections with international alumni.

Conclusion

As we move into 2025, higher education institutions must navigate a complex landscape shaped by shifting student mobility patterns, regulatory changes, and evolving geopolitical dynamics. By focusing on employability outcomes, enhancing support for international graduates to find employment back home, and leveraging data to inform strategy, universities can position themselves for success in an increasingly competitive global market.

While the challenges are significant, they also present opportunities for innovation and growth. By addressing the needs and motivations of diverse student populations and adapting to changing circumstances, higher education institutions can chart a course through the choppy waters ahead and emerge stronger on the other side.

--

ENTREPRENEUR DATA

ACG Entrepreneur Data: Key Insights on Graduate Employability in the Entrepreneurial Landscape

As we explore the evolving world of entrepreneurship, it’s essential to understand the role that employability plays in shaping the entrepreneurial journey. In this section, we dive into ACG Entrepreneur Data, offering key insights into the employability trends among international graduates and their path to entrepreneurship. With a focus on real-world outcomes, we aim to highlight how graduates are navigating the transition from education to entrepreneurial ventures, and the impact this has on today’s business landscape.

- GENERAL DATA -

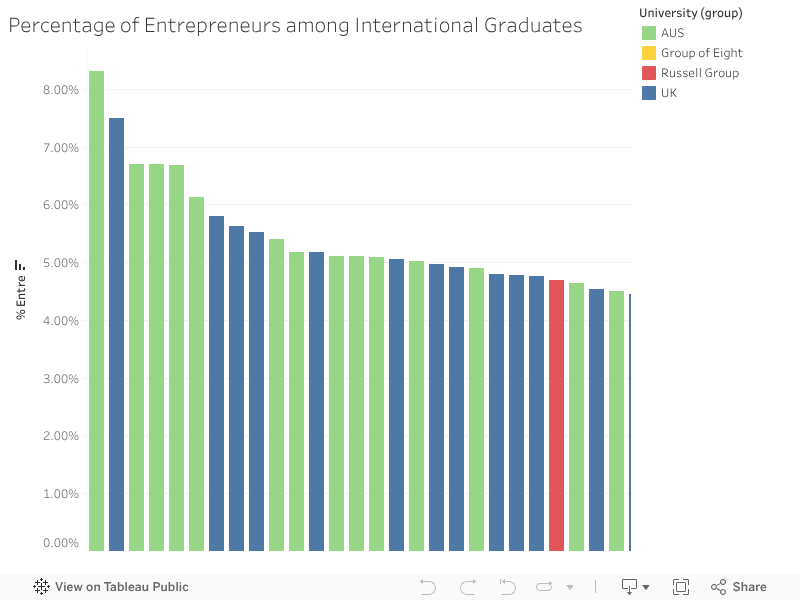

The graph above illustrates the percentage of entrepreneurs among international graduates. The first half shows that the majority of standard UK and Australian institutions have entrepreneurship rates ranging from 8.31% to 3.66%, with only one Russell Group member at 4.68%. In contrast, the second half of the graph shows that Russell Group and Group of Eight institutions tend to have lower entrepreneurship rates, indicating that these institutions generally exhibit less entrepreneurial activity.

The second graph shifts the focus to the number of entrepreneurs among these graduates. While the UK still leads in the total number of entrepreneurs, followed by Australia, there is an interesting exception. One Russell Group institution stands out, showing a relatively high number of entrepreneurs despite its lower percentage rate. This indicates that while entrepreneurial activity may be less concentrated in Russell Group institutions, the absolute number of entrepreneurs can still be significant in some cases.

Meanwhile, Australia shows a higher concentration of entrepreneurs compared to the UK, but with fewer total entrepreneurs overall. The Group of Eight institutions, in terms of both concentration and total count, are positioned similarly in both graphs, indicating a relatively consistent level of entrepreneurial activity across both percentage and number.

Note: we can identify individual entrepreneurs on behalf of your institution if you become an ACG’s university partner.

Based on our ACG data, collected specifically from international graduates, we’ve identified key trends in the entrepreneurial landscape. Among all regions, India stands out with the largest proportion of entrepreneurs, accounting for 30.67% of the total. Following India, Malaysia and Indonesia each represent 10.71%, while Singapore comes in at 10.68%, and China at 10.06%.

Overall, entrepreneurs make up 3.55% of all graduates in our dataset. While this percentage may seem relatively modest, it reflects the growing number of graduates pursuing entrepreneurial ventures after their studies.

Additionally, when examining the origin countries of these entrepreneurial graduates, we see that a significant 58.50% of them graduated from the UK, while 35.42% graduated from Australia. These trends underscore the important role these educational hubs play in nurturing future entrepreneurs, particularly in the context of international graduates returning to their home countries to start their own businesses.

In Australia, there is a higher concentration of entrepreneurs, with 3.97% of Australian international graduates identifying as entrepreneurs, compared to 3.31% of UK graduates. Interestingly, the United States surpasses Australia with a slightly higher percentage of entrepreneurially inclined graduates, at 4.09%.

Distribution of Entrepreneurs by Degree and Level of Study

Among the 3.55% of international graduates who become entrepreneurs, the majority pursued Business degrees (52.68%), followed by STEM degrees (25.46%) and Other degrees (21.86%).

In Australia, a higher percentage of entrepreneurs studied Business degrees, at 55.74%, compared to the UK, where the figure stands at 51.65%. However, the UK has a slightly higher proportion of entrepreneurs with STEM degrees, with a 1.26% difference. When looking at the US, there is a significant difference: 34.07% of US entrepreneurs have STEM backgrounds, while the percentage of entrepreneurs with Business degrees is lower.

This variation in educational backgrounds may help explain why the US has a larger share of tech startups compared to Australia and the UK, as there is a greater emphasis on STEM education among US entrepreneurs. However, it’s important to recognize that while educational background plays a role, other factors may also contribute to the entrepreneurial landscape in each country, and this correlation doesn’t necessarily imply causation.

Entrepreneurial education levels globally are fairly balanced, with 49.87% of entrepreneurs holding undergraduate degrees and 48.39% holding postgraduate degrees. As noted in our previous issue on Indian entrepreneurs, a higher proportion of Indian graduates (65.61%) pursue postgraduate degrees.

In Australia, 54.47% of entrepreneurs have undergraduate degrees, compared to 46.36% in the UK—an 8.11% difference. While the UK leads with 9.35% of entrepreneurs holding postgraduate degrees, Australia surpasses the UK by 1.24% in entrepreneurs with Doctoral degrees.

Key highlights from the summary table on entrepreneurial distribution by education level and degree:

- Doctorates and Entrepreneurship: In the UK, most entrepreneurs with Doctorates pursued niche or specialized degrees, while in Australia, Doctorate holders are more likely to have studied Business-related fields.

- Undergraduate vs. Postgraduate Entrepreneurs: Australia has a higher proportion of entrepreneurs with undergraduate degrees, while the UK shows a greater percentage of postgraduate entrepreneurs.

- STEM Degree Representation: Both regions show relatively low representation of STEM graduates among entrepreneurs, suggesting a potential gap in entrepreneurial activity in technical fields, which could impact innovation and startup growth in those sectors.

- EMPLOYMENT DATA -

1. Average Employability Figures

This section presents the ACG average employability rates for entrepreneurs, comparing these figures with overall employment trends.

Employability Comparison: Entrepreneurs vs. the Average

Entrepreneurs have an impressive employability rate of 96%, significantly higher than the overall average of 80.65%.

Note: While 96% of entrepreneurs are employed—whether through their own ventures or other professional roles—the remaining 4% may represent former entrepreneurs who are no longer actively running businesses. This group could include individuals who have exited their ventures, are in transition, or have opted to retire or pursue other interests.

Entrepreneur Employability by Country of Graduation

Both Australia and the UK show high employability rates for entrepreneurs, with Australia leading at 96.19% compared to the UK’s 95.71%. Australia also has a higher overall employability rate at 83.21%, while the UK’s overall rate stands at 79.12%.

Entrepreneur Employability by University Group

The entrepreneurial employability rates are impressively high across all university groups, ranked as follows: AUS leads at 96.37%, followed closely by UK universities at 95.93%, then the Russell Group at 95.33%, and finally the Group of Eight at 95.24%.

These ranking highlights that, regardless of university prestige, entrepreneurs enjoy strong employability prospects, indicating the resilience and adaptability of entrepreneurial skills in the job market.

Additionally, if compared between overall employability and entrepreneurial employability, the UK exhibits the highest disparity (17.08%), indicating that graduates in this region may have particularly strong entrepreneurial skills relative to their overall job market readiness. In contrast, the Group of Eight exhibits the smallest difference (12.87%), indicating a tighter correlation between overall employability and entrepreneurial employability within that group.

Entrepreneur Employability by University

Entrepreneurs from Australian universities exhibit a range of employability outcomes, with some achieving high rates and others lower. Among the top 5 universities for entrepreneurial employability, 3 are Australian, 2 are from the UK, and 1 is from the Russell Group. In the top 10, representation is evenly split, with 5 universities from Australia and 5 from the UK, 3 of which belong to the Russell Group. This reflects strong competition between Australian and UK institutions, with Australian universities slightly outperforming their UK counterparts.

The gap between the highest and lowest employability rates is 16.67%.

Comparative Analysis of Entrepreneurial Employability and Graduate Employability by University

In the comparative graph of overall average employability versus entrepreneurial average employability, only one university—an Australian institution—shows lower entrepreneurial employability than the overall average (by 0.23%).

After accounting for outliers, Australian universities generally show higher employability for their entrepreneurs compared to the average employability of their graduates. This aligns with the earlier data, where Australia ranked highest in entrepreneurial employability at 96.37%. In contrast, UK universities and those in the Russell Group exhibit a smaller disparity between the employability of entrepreneurs and that of other graduates, reflecting the UK's more balanced entrepreneurial skill set as compared to overall job market readiness. Notably, 7 universities have lower employability for their entrepreneurs than the average: 3 from Australia, 3 from the Russell Group, and 1 from the UK.

2. Average Time Taken to First Job (in Months)

This section examines the average time it takes for entrepreneurs to either enter employment or launch their own ventures after graduation, offering insights into the speed of entrepreneurial activity compared to general graduate trends.

By Country of Graduation

Entrepreneurs from the UK secure their first job more quickly than those in other regions, although their time to employment is slightly slower than the overall average—by less than two weeks. In contrast, entrepreneurs from Australia enter the workforce faster than their non-entrepreneurial peers, highlighting a more immediate transition into employment or ventures.

By University Group

Graduates from Australia's Group of Eight universities take the shortest time to secure their first job or entrepreneurial opportunity, averaging 19 months. Entrepreneurs from this group are even quicker, at 17.5 months.

Conversely, entrepreneurs from the UK's Russell Group take longer, with an average time of 21.5 months, compared to the overall graduate average of 19.6 months.

For both Australia and the UK, overall graduates and entrepreneurs take a similar amount of time to start their careers or ventures, with Australian graduates averaging 24 months and UK graduates 20 months.

By University

Entrepreneurs from UK universities tend to have the shortest time to secure their first job or launch their ventures, with two Australian universities also performing well in this regard. However, when considering the broader landscape, the majority of entrepreneurial graduates from Australia’s Group of Eight universities—specifically 6 out of 8—are able to enter the workforce or start their businesses more quickly. The Russell Group also shows strong performance in this area, indicating that certain prestigious universities may offer advantages for aspiring entrepreneurs, though not all do.

Just over 50% of universities see entrepreneurs entering the job market or launching ventures faster than their non-entrepreneurial peers, with most of these universities located in Australia. In contrast, universities where entrepreneurial graduates face greater challenges in securing jobs tend to be concentrated in the UK and the Russell Group.

Note: Not all 40 universities included in the analysis have data on entrepreneurial graduates, which is why fewer than 40 Australian universities are represented in the graph.

3. Annual Salary (£)

In this section, we explore the salary trends among entrepreneurs, comparing their earnings to those of their non-entrepreneurial peers. Understanding these figures provides valuable insights into the financial outcomes of pursuing entrepreneurial ventures, as well as the broader economic impact of entrepreneurship across regions and university groups.

Average Salaries and Entrepreneurial Salaries

The average annual salary for entrepreneurs stands at approximately £13,558, significantly lower than the average salary of £22,126. This disparity highlights the financial challenges entrepreneurs may face, particularly in the early stages of their ventures, compared to those in more traditional employment roles.

Average Salaries and Entrepreneurial Salaries by Country

The majority of entrepreneurs earn less than the average salary in their respective regions, with the notable exception of China, where entrepreneurs earn slightly more—approximately £2,000 above the average.

In comparison, Singaporean entrepreneurs earn the most among all regions at nearly £42,000, followed by Hong Kong at approximately £37,000, and China at nearly £31,000. Malaysian entrepreneurs, however, rank fourth with an average salary of only about £10,000, resulting in a substantial gap of £21,000 compared to their Chinese counterparts.

Average Salaries and Entrepreneurial Salaries by Country of Graduation

The average annual salary is approximately £26,000 in the US, £22,000 in both New Zealand and the UK, and £21,600 in Australia. Entrepreneurs in the US and New Zealand earn an average of £20,000, which is respectively, £6,000 and £2,000, less than the average salary in their countries. In contrast, entrepreneurs in Australia and the UK see a significant decline in earnings, with an average salary of just £13,000. This highlights a considerable gap, where entrepreneurs in these regions earn notably less than their non-entrepreneurial peers, particularly in Australia and the UK.

Average Salaries and Entrepreneurial Salaries by Country of Origin and Country of Graduation

The table offers a comparative overview of the average annual earnings of entrepreneurs based on their graduation from either Australia or the UK. Key insights include:

- Entrepreneurs in Singapore, Hong Kong, Malaysia, Thailand, and Indonesia tend to earn more if they graduated from Australia rather than the UK.

- Conversely, in countries such as China, Vietnam, and Pakistan, those who graduated from the UK have higher earnings.

- In India, the earnings difference between those who graduated from Australia versus the UK is minimal, with just a £2 discrepancy on average.

Average Salaries and Entrepreneurial Salaries by Degree

The data compares average salaries across different degree fields, distinguishing between the general workforce and entrepreneurs. On average, entrepreneurs in STEM fields earn the highest, with a salary of £14,109, followed closely by those in "Other" sectors at £14,088. Entrepreneurs in Business earn the lowest, with an average salary of £13,006.

For the general graduate workforce (including both entrepreneurs and non-entrepreneurs), the highest average salary is found in the "Other" sector at £23,012, followed by STEM graduates at £21,954 and Business graduates at £21,877. Once again, Business graduates earn the least. The "Other" sector stands out for its higher average salary, which may reflect the inclusion of professions such as law, film production, theatre studies, and anthropology—fields where established professionals in senior roles tend to earn significantly more.

Average Salaries and Entrepreneurial Salaries by Level of Study

According to our ACG data, postgraduates earn the least on average compared to undergraduates and doctorates. A similar trend is observed among entrepreneurial graduates, with undergraduates earning the second-highest income, and doctorates earning the highest. However, across both overall graduates and entrepreneurial graduates, entrepreneurs consistently earn less than the average graduate, highlighting a financial disparity in entrepreneurial careers.

Average Salaries and Entrepreneurial Salaries by Degree and Level of Study

The following tables present average annual salaries by degree and level of study. Key highlights include that, overall, doctorate holders with business degrees earn the highest salaries, while entrepreneurs with doctorate-level niche degrees earn the most among all entrepreneurial graduates. Additionally, STEM postgraduates tend to earn the least.

We encourage a closer examination of the data to uncover more detailed trends. Please note that these figures are based on data collected by Asia Careers Group Sdn. Bhd. and may not fully reflect broader market conditions.

Average Entrepreneurial Salaries by University

The graph shows that entrepreneurial graduates from Russell Group universities have the highest average annual salaries, followed second by graduates from a UK university. There is a slight drop in earnings thereafter, with graduates from Australia’s Group of Eight universities ranking third, and another Australian university coming in fourth– which reinforces the earlier observation that Australian entrepreneurial graduates tend to earn slightly less on average than their UK and Russell Group peers. In the overall salary distribution, most Australian universities fall in the middle range, while the highest earners are predominantly from the Russell Group, the Group of Eight, and other UK institutions.

Average Salaries and Entrepreneurial Salaries by Industry Popularity Rank

Top 6 Highest-Earning Industries for Entrepreneurs:

- Others: £25,629

- Sports and Fitness: £19,495

- Design, Fashion and Graphics: £18,713

- FMCG: £18,604

- Engineering: £18,113

- Finance: £17,141

Top 6 Most Popular Industries Among Entrepreneurs:

- IT

- Education and Research

- Finance

- Design, Fashion and Graphics

- FMCG

- Healthcare

- KEY TAKEAWAY -

GENERAL DATA - Data Summary

|

General Demographics of Entrepreneurs

|

|

Entrepreneurial Qualifications: Degree and Level of Study

|

EMPLOYMENT DATA - Data Summary

|

1. Employability

|

|

2. Average Time to First Job or Venture:

|

|

3. Annual Salary Comparison (£)

|

By reviewing this summary, you will gain valuable insights into the key trends and disparities within the entrepreneurial landscape, including variations in earnings, employability, and the influence of educational backgrounds. The findings presented offer a broad overview, but we encourage you to revisit the data section for a more comprehensive understanding of the patterns and nuances discussed.

This concludes the data section for entrepreneurs, based on our ACG data.

--

Starting the New Year as We Mean to Go On – The Power of Innovation and Start-ups

The job market for recent and soon-to-be graduates remains bleak as economic uncertainty, accelerated by the pandemic and the impacts of the Fourth Industrial Revolution, reshapes hiring practices. With just-in-time recruitment, digitisation, and the rise of artificial intelligence, the employment landscape is evolving rapidly. Against this challenging backdrop, a new type of career guidance is emerging, aimed at helping graduates navigate an increasingly unpredictable and complex (often called "VUCA" – volatile, uncertain, complex, and ambiguous) world.

Just a few years ago in 2022, graduate job fairs on and offline were bustling events. Students and employers alike would flock to these virtual and in person gatherings, each in search of their ideal match. It was, to use an old saying, “like shooting fish in a barrel” for employers, who had easy access to a concentrated group of job-ready students. Now, with widespread layoffs particularly from the FAANGs (Meta (formerly known as Facebook); Amazon; Apple; Netflix; and Alphabet (formerly known as Google) & a significant drop in job availability in other sectors, including consulting and finance, the process feels more akin to a game of “Go Fish”—where guesswork, strategy, and the occasional stroke of luck are required to find a position.

The Institute of Student Employers (ISE) survey revealed that, over the past year, employers received more than 1.2 million applications for just under 17,000 graduate positions—an average of about 140 applications per role. This represents a 59% increase from the previous year, marking the highest number of applications per job since the ISE began tracking the data in 1991.

While graduate vacancies have seen a modest 4% growth this year, employers are projecting only a 1% increase next year, largely due to ongoing economic challenges. “The current job market is tough for graduates, with a considerable jump in applications per vacancy,” said Stephen Isherwood, joint chief executive of the ISE.

Some companies are receiving 200 applications per position and there is fierce competition for work experience and internships—experiences that students must secure while at university to stand a chance of landing a good job after graduation. Jonathan Black, head of the careers service at University of Oxford, said that the number of graduate vacancies on its website is at an all-time low. “We have seen a big drop in the number of graduate vacancies this year compared with last — from 9,000 live vacancies on our system to just 6,000.”

The situation has also exacerbated longstanding issues, including graduate overqualification and the mismatch between degrees and available jobs. According to the Chartered Institute of Personnel and Development, the influx of overqualified graduates has reached a "saturation point," often pushing less qualified workers out of positions. Given the government’s projection that nearly half of UK graduates may never earn enough to repay their student loans, the sustainability of this “conveyor belt” approach to higher education is under scrutiny.

Unfortunately, this troubling trend is not confined to the UK. A report by the Institute of Student Employers, published in summer 2020, found that the pandemic’s impact on graduate recruitment is global, with countries worldwide experiencing a rise in youth unemployment—disproportionately affecting young people. As a result, higher education institutions are being forced to rethink their approach to career services.

The Need for Reinventing Career Services

As far back as 2013, career development expert Andy Chan, Vice President for Innovation and Career Development at Wake Forest University, called for a complete overhaul of college career services. In his TEDx talk, “Career Services Must Die,” he argued that universities should treat career development as a core part of education, not as an auxiliary student service. He revisited his message seven years later, disappointed that little had changed in most institutions. While many colleges have merely maintained the status quo, some are beginning to innovate in response to the unprecedented challenges graduates face today.

A New Approach to Careers Education

There is no one-size-fits-all solution, but some guiding principles could reshape how careers education is delivered in universities:

- Inclusive Support for All Students: Career services should support every student equally, irrespective of their background, nationality, gender, disability, or orientation. This inclusivity must extend to both students from the country of study and international students who may return home after graduation.

- Data-Driven and Personalized Guidance: Career guidance must be informed by robust data on graduate outcomes, employability metrics, and labour market trends both locally and in key overseas markets, such as China and India. Personalised career advice tailored to each student’s aspirations, including where they wish to work, can help align students’ expectations with reality.

- Expanded Horizons: Students should be encouraged to look beyond traditional roles and industries. Not all finance jobs are at banks, and not every tech position is in Silicon Valley. Students must also be reminded that companies often prioritize an applicant’s adaptability, resilience, and work experience over their degree discipline.

- Unadvertised Opportunities: Networking skills, account mapping, and outreach techniques can be invaluable for uncovering positions that are not openly advertised. As more graduates must become “job makers” rather than just “job takers”, they will need tools to identify and create employment opportunities that align with their skills and goals.

- Fostering Entrepreneurial Thinking: As the gig economy grows, students need to think beyond traditional employment. Freelancing, startups, and self-employment are increasingly viable career paths that provide valuable experience and cultivate skills like resourcefulness and business acumen—qualities that are highly valued by employers.

Supporting Women Entrepreneurs in Higher Education

In addition to developing a broader range of skills, universities need to play a more active role in nurturing young entrepreneurs—particularly women, who face unique challenges in the startup ecosystem. Elizabeth Holmes, the disgraced founder of Theranos, once said that young women should strive for excellence in STEM fields. Despite her subsequent legal issues, her words ring true. Holmes' trial may indeed be a cautionary tale, but it also brings to light the persistent biases against women in entrepreneurship, which universities have a duty to address.

One common critique of Holmes is that her high-profile failure could discourage young women from founding companies. However, her story should not be used as a reason to stifle women’s entrepreneurial ambitions. The issue with Holmes’s case isn’t that she dropped out of college—many male tech founders, such as Mark Zuckerberg, Bill Gates, and Steve Jobs, did the same and are celebrated for their innovations. The problem lies in the specific circumstances surrounding her rise and fall, including the ethical and legal issues at play. Holmes’s story is not a cautionary tale about entrepreneurship—it’s a reminder of the challenges women face in a biased ecosystem that often judges them more harshly than their male counterparts.

Some universities are beginning to step up to the challenge. Programs like Imperial College London’s WE Innovate aim to support female entrepreneurs through funding, mentorship, and networking opportunities. Similarly, universities such as the University of Winchester and the University of Suffolk are also running initiatives designed to empower women entrepreneurs. These efforts are commendable, yet they remain the exception rather than the rule. For meaningful progress, higher education needs to embed entrepreneurial skills into all degree programs, making them accessible to all students, not just those pursuing business degrees.

Preparing All Graduates for a Changing World

Given the increasing automation of jobs, the expansion of the gig economy, and employers’ concerns about graduates lacking essential skills, the traditional focus of career services on resume writing and interview prep is no longer sufficient. Instead, career curricula should emphasize creative problem-solving, entrepreneurial thinking, and the ability to market one’s ideas effectively.

Higher education has both an opportunity—and a responsibility—to equip graduates with these critical skills. Some institutions are experimenting with initiatives like “T-Groups,” a concept from Stanford that fosters self-awareness and interpersonal skills, or by creating networks with local businesses to encourage cross-collaborative innovation. These types of initiatives could help young entrepreneurs develop products, launch startups, and navigate the ethical considerations that come with running a business.

Learning from Cautionary Tales

Holmes' rise and fall illustrate the importance of ethical leadership in entrepreneurship. As universities strive to equip students with the skills to thrive in complex markets, they must also instil strong ethical principles. In Silicon Valley’s culture of “fake it until you make it,” the pressure to meet investors’ high expectations can lead to moral compromises, as seen in Holmes’ case.

To avoid repeating these mistakes, higher education must provide young entrepreneurs with both a moral and an economic compass. Learning from Holmes’ story does not mean discouraging ambition; rather, it’s about encouraging students to pursue it responsibly and ethically.

The Future of Career Services and University Support for Graduates

As the job market continues to evolve, universities must evolve with it. It’s time to go beyond traditional career services and embrace a more comprehensive, innovative approach —one that equips students with the knowledge, skills, and ethical grounding they need to succeed. Whether through improved data-driven career guidance, stronger support for entrepreneurs, or a greater emphasis on transferable skills, universities have a critical role to play in helping students navigate the complex labour market.

In the end, higher education institutions should empower students to become both job makers and job takers—prepared to seize opportunities as they arise, or to create their own. The stakes are high, and the work is urgent. The job market of tomorrow will be far more like “Go Fish” than “shooting fish in a barrel,” but with the right support, today’s graduates will be well-equipped to thrive.